CATL vs BYD: Two titans define the EV battery era

Comparison of the two

CATL and BYD control 55% of the global EV battery market, yet pursue fundamentally different strategies that matter profoundly for investors. CATL dominates as the world's largest third-party battery supplier with 37.9% global market share and customers ranging from Tesla to BMW, while BYD leverages vertical integration to produce batteries primarily for its own vehicles—making it the world's largest EV manufacturer in 2025. Both companies have achieved breakthrough ultra-fast charging technologies and are racing toward solid-state battery commercialization, targeting initial deployment in premium models by 2027, but their distinct business models create different risk-reward profiles for value investors evaluating the EV supply chain.

CATL commands the premium segment with unmatched scale

Contemporary Amperex Technology Co. Limited was founded in December 2011 in Ningde, Fujian Province by Robin Zeng Yuqun, who previously co-founded ATL (Amperex Technology Limited)—the company that became Apple’s iPod battery supplier. CATL went public on the Shenzhen Stock Exchange in June 2018 at a valuation of $12.3 billion and completed a Hong Kong secondary listing in May 2025, raising HK$41 billion ($5.2 billion) in what became the largest global IPO of 2025.

The company has maintained its position as the world’s #1 EV battery maker for eight consecutive years, with 2024 installations reaching 339.3 GWh—more than double its nearest competitor. CATL’s domestic market share stands at 45.08% in China, while it holds 68% of China’s NCM battery market and 37.2% of the LFP segment. In energy storage systems, CATL commands 36.5% global share, reinforcing its “second growth curve” strategy.

CATL’s customer roster reads like a who’s who of global automaking: Tesla (its largest customer, with a supply agreement through December 2025), BMW (a strategic partner since 2012 with a €4 billion supply deal), Mercedes-Benz, Volkswagen Group, Stellantis, Ford (technology licensing), Honda, Hyundai, and virtually every major Chinese EV brand including NIO, Li Auto, Xpeng, Geely/Zeekr, and Xiaomi. As of November 2024, CATL batteries powered over 17 million vehicles globally.

Financial performance reveals pricing pressure but improving margins

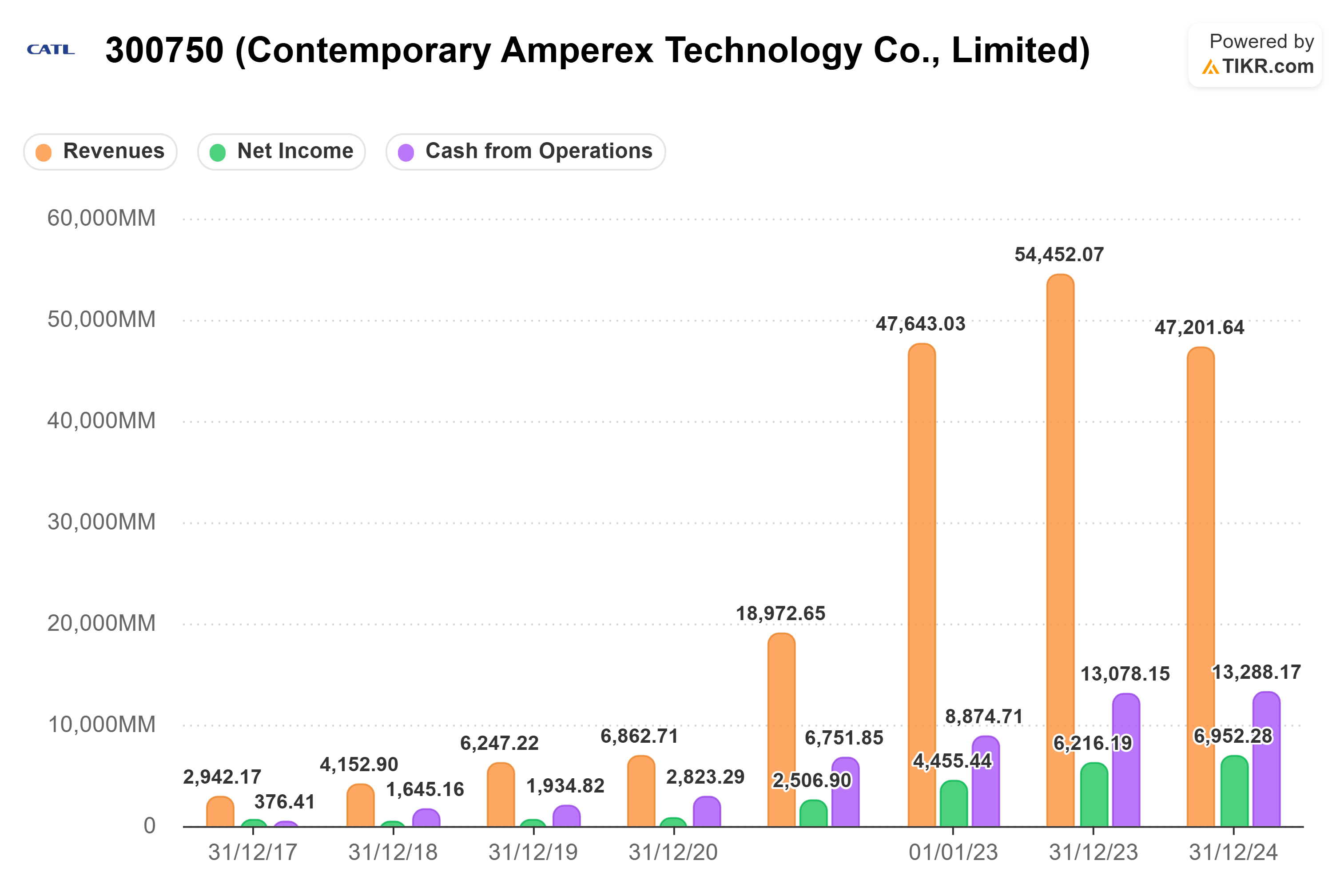

CATL reported its first-ever revenue decline in 2024, with full-year revenue falling 9.7% to RMB 362 billion (~$52 billion) from RMB 401 billion in 2023. However, this headline figure masks a more nuanced story. The decline resulted primarily from lithium carbonate prices falling from 100,000 yuan/ton to 75,000 yuan/ton, which drove average power battery selling prices down 25.3% from 0.889 yuan/Wh to 0.664 yuan/Wh.

Despite lower revenue, CATL’s profitability improved significantly. Net profit attributable to shareholders rose 15% to RMB 50.7 billion (~$7 billion), while comprehensive gross margin expanded 5.3 percentage points to 24.4%. The company’s Q3 2024 gross margin hit a record 31.17%, demonstrating pricing power with upstream suppliers even as it passed lower material costs to customers. Overseas business margins reached 29.45%, nearly 10 percentage points higher than the prior year.

CATL revenues, net income and cash flow from operations

CATL maintains over RMB 300 billion in cash reserves and declared a dividend of RMB 45.53 per 10 shares (approximately 50% payout ratio). The company employs over 20,000 R&D staff across six global research centers, holding 43,354 patents worldwide.

Global manufacturing expansion accelerates across three continents

CATL operates 15 battery manufacturing plants worldwide with installed production capacity of 646 GWh—the highest globally. In China, major facilities include the flagship Ningde headquarters (120 GWh capacity), along with plants in Liyang, Yibin (the world’s first zero-carbon battery factory), Shanghai, Zhaoqing, Xiamen, and the newly operational Jining facility in Shandong (60 GWh Phase 1, expanding to over 100 GWh by 2026).

International expansion represents CATL’s most significant strategic initiative, with committed investments exceeding €17 billion ($19+ billion) across four major projects:

Hungary (Debrecen): CATL’s largest international project involves a €7.3-7.6 billion investment for a 100 GWh facility. Module assembly began in 2024, with full cell production expected in March-April 2026. Phase 1 capacity will reach 30-40 GWh by end of 2025. The plant will serve Mercedes-Benz and BMW, which is building its own facility nearby.

Germany (Erfurt): CATL’s first non-China plant began operations in December 2022 with €1.8 billion invested and 8-14 GWh capacity. The facility turned profitable in 2024 and serves BMW, Volkswagen, and Daimler. CATL has canceled expansion plans here to focus resources on Hungary.

Spain (Zaragoza): A 50-50 joint venture with Stellantis announced in December 2024, with €4.1 billion investment for 50 GWh of LFP battery capacity. Construction started November 2025, with production expected late 2026.

Indonesia: A $6 billion integrated project with Indonesia Battery Corporation covering the full value chain from nickel mining to battery recycling. Production is expected by end of 2026, with ultimate capacity of 40 GWh.

The Hong Kong IPO allocated approximately 90% of proceeds to the Hungary project, underscoring the strategic importance of European localization amid EU tariffs of 38% on Chinese-made EVs.

Battery technology spans the full spectrum from LFP to condensed matter

CATL offers the industry’s most comprehensive battery portfolio, spanning multiple chemistries and form factors. In NCM/NMC ternary batteries, CATL produces NCM811 cells achieving 280-304 Wh/kg energy density at cell level, alongside NCM622 (220-230 Wh/kg) and NCM523 (160-200 Wh/kg) variants. The company’s premium Qilin Battery (CTP 3.0) achieves 255 Wh/kg pack-level energy density for NMC chemistry and 160 Wh/kg for LFP—enabling 1,000+ km range in vehicles like the Zeekr 009.

CATL has invested heavily in LFP technology through its Shenxing battery family, directly challenging BYD’s Blade Battery dominance:

Shenxing (August 2023): World’s first 4C superfast charging LFP, delivering 700+ km range and 400 km in a 10-minute charge

Shenxing PLUS (April 2024): First LFP to exceed 1,000 km range with 205 Wh/kg pack density—breaking the 200 Wh/kg LFP barrier

Shenxing 2nd Generation (April 2025): Achieves 12C peak charging rate with 1.3 MW peak power, enabling 520 km range in just 5 minutes of charging

Shenxing Pro (September 2025): Offers 758 km WLTP range with 12-year/1,000,000 km lifespan and just 9% degradation after 200,000 km

The company’s Naxtra sodium-ion battery represents another breakthrough, achieving 175 Wh/kg energy density—the highest among sodium-ion globally—with 500+ km range for passenger EVs. Mass production begins December 2025, offering a cost-effective alternative as lithium prices recover.

BYD’s Blade Battery and vertical integration create a different moat

BYD’s approach differs fundamentally from CATL’s third-party supplier model. Founded in 1995 as a battery manufacturer before expanding into automobiles in 2003, BYD controls nearly every aspect of its value chain—from lithium mining partnerships in Chile, Africa, and Brazil to battery cells, electric motors, semiconductors, power electronics, and vehicle assembly. This “full stack” integration delivered remarkable resilience during the 2021-2022 chip shortage, when BYD’s sales surged over 200% while competitors lost millions in production.

The Blade Battery, launched in March 2020, exemplifies BYD’s LFP expertise. The distinctive 96 cm long cell format achieves 165 Wh/kg cell-level density (140-150 Wh/kg pack level) with 50% better space utilization than traditional block batteries. BYD’s nail penetration test became legendary in the industry—the Blade Battery reached only 30-60°C after penetration with no smoke or fire, while NCM batteries exceeded 500°C and violently burned.

LFP’s inherent safety advantages underpin BYD’s positioning. The chemistry’s olivine crystal structure holds oxygen tightly, preventing the thermal runaway that releases oxygen in NCM batteries to feed combustion. LFP cells release 75-85% less heat energy than comparable NMC cells, with thermal runaway onset at 220-260°C versus 170-210°C for NCM. Industry data shows 5-6× fewer thermal events per million miles for LFP versus traditional lithium-ion.

Blade Battery 2.0, expected in 2025, promises a 40% energy density increase to 160-210 Wh/kg, charging rates exceeding 5.5C, and 15% lower production costs. BYD’s revolutionary Super e-Platform (March 2025) delivers 10C charging with 1 MW peak power, enabling 400 km range in just 5 minutes—comparable to CATL’s Shenxing 2nd Generation performance.

Technology roadmaps converge on solid-state by 2027

Both companies are racing toward solid-state battery commercialization with remarkably similar timelines. CATL has invested over 10 billion yuan with approximately 1,000 dedicated researchers, achieving 500 Wh/kg in prototype cells using sulfide electrolyte technology. The company targets small-batch solid-state production by 2027 and large-scale commercialization by 2030.

CATL’s condensed matter battery, unveiled in April 2023, achieves 500 Wh/kg energy density—nearly double typical lithium-ion at 250-300 Wh/kg. This technology uses a biomimetic gel-like electrolyte between liquid and solid-state and is already powering electric aircraft in aviation applications. A 4-ton electric aircraft completed testing in 2024, with 8-ton models expected by 2027-2028.

BYD began solid-state research in 2013 and produced first cells (20-60 Ah capacity) in 2024. The company targets 400 Wh/kg energy density—below CATL’s 500 Wh/kg target—with demonstration vehicles by 2027 and mass production by 2030. BYD aims for “solid-liquid parity” on costs by 2030 through 15-20× cost reductions.

Competitive dynamics reveal complementary rather than zero-sum positioning

Despite their rivalry, CATL and BYD largely serve different market segments. CATL dominates the premium segment with an estimated 70%+ market share in vehicles priced above $35,000, supplying technology-leading batteries to luxury and performance-oriented OEMs. BYD focuses on mass-market vehicles through its own brands (BYD, Denza, Yangwang), with approximately 90% of battery production consumed internally and only 20% sold externally to partners like Toyota.

Global market share data shows CATL maintaining a consistent 20+ percentage point lead over BYD: 37.9% versus 17.2% in 2024, expanding slightly to 38.1% versus 16.9% through October 2025. In China, the combined CATL-BYD duopoly controls approximately 69.5% of the domestic market.

Both face significant industry headwinds. Chinese battery manufacturers project 4,800 GWh of capacity by 2025 against approximately 1,200 GWh of demand—a 4× overcapacity suggesting massive consolidation ahead among the nearly 50 Chinese battery makers. Price wars have reached “disturbing” levels according to regulators, while geopolitical tensions continue escalating. CATL was added to the U.S. Pentagon’s “Chinese military companies” list in January 2025, effectively barring direct U.S. market participation beyond technology licensing arrangements like its Ford partnership.

Investment thesis depends on exposure preferences and risk tolerance

For value investors, CATL offers exposure to the broader EV battery ecosystem through diversified customer relationships, technological leadership across multiple chemistries, and strong international expansion. The company’s 24.4% gross margins, RMB 300+ billion cash position, and growing services revenue (battery swapping, data analytics) support premium valuation. Key risks include geopolitical exposure, OEM in-sourcing trends, and reliance on Chinese and European markets.

BYD offers a vertically integrated EV-plus-battery investment with direct exposure to vehicle sales growth. The company sold 4.27 million NEVs in 2024, overtook Tesla as the world’s largest EV manufacturer in 2025, and targets 50% of sales outside China by 2030 (from approximately 10% today). BYD’s cost leadership through integration provides margin protection in price wars, while its safety-focused LFP positioning aligns with regulatory trends. Key risks include China concentration, quality perception challenges in Western markets, and margin pressure from aggressive pricing strategies.

The global EV battery market is projected to grow from approximately $61 billion in 2024 to $199-496 billion by 2030, with battery demand exceeding 3 TWh annually by 2030 versus approximately 1 TWh today. LFP chemistry now commands 79.4% of the Chinese market, favoring both companies’ investments in ultra-fast charging LFP technology while their parallel solid-state development hedges against longer-term chemistry shifts.

Conclusion: Distinct paths to the same electrified destination

Distinct paths to the same electrified destination CATL and BYD represent two viable but fundamentally different approaches to capturing value in the EV transition. CATL’s pure-play supplier model generates higher margins and capital efficiency by focusing exclusively on battery technology, though it depends on OEM relationships and faces intensifying geopolitical restrictions. BYD’s extensive vertical integration creates a formidable cost moat and direct consumer relationship but concentrates operational risk in a single company’s execution across mining, chips, batteries, and vehicle manufacturing.

For investors seeking dedicated technology exposure with superior profitability, CATL offers the clearer play despite near-term revenue pressure from falling battery prices. For those preferring integrated EV exposure with cost leadership and vehicle growth optionality, BYD presents a compelling alternative. The most important insight for value investors may be that both companies’ solid-state timelines, ultra-fast charging achievements, and capacity expansion plans suggest the industry’s technology trajectory is converging—making execution quality and capital allocation discipline the ultimate differentiators over the coming decade.

Disclaimer: This is not investment advice. Do your own research. Cyclical industries can be volatile.

Very good structured summary. Thank you.