The Capital Efficiency Compounder: A Comprehensive Investment Thesis on ConocoPhillips

The Evolution of the "Super-Independent"

In the complex and often volatile world of global energy markets, ConocoPhillips (COP) has carved out a unique identity that defies traditional categorization. It is neither a massive Integrated Major—burdened by sprawling downstream refining and chemical networks—nor is it a typical nimble Independent, often constrained by single-basin exposure and balance sheet fragility. Instead, ConocoPhillips operates as a “Super-Independent,” a hybrid entity that combines the scale, balance sheet fortitude, and global reach of a Major with the operational agility and upstream focus of an Independent.

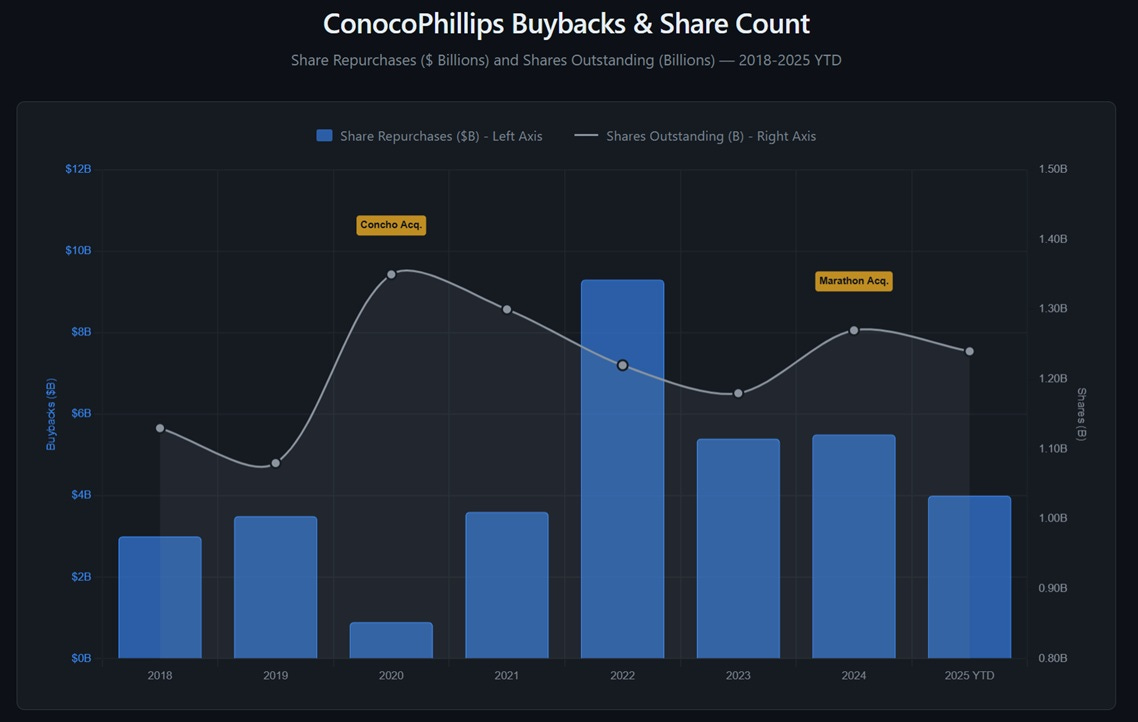

ConocoPhillips has transformed itself into the world’s largest independent oil and gas company through disciplined acquisitions, roughly doubling production from 1.1 million barrels of oil equivalent per day (boe/d) in 2020 to 2.4 million boe/d today, while limiting share dilution to just 17% through aggressive buybacks. The company trades at $93.69 per share with an EV/EBITDA of 5.2x—a 15-25% discount to integrated majors—and offers exposure to a powerful long-term trend: explosive electricity demand from AI data centers that will drive natural gas consumption for decades.

COP’s investment thesis rests on three pillars: an ultra-low cost base with breakeven around $35 per barrel, a growing LNG portfolio targeting 10-15 million tons per year capacity, and $10 billion in annual shareholder returns.

How COP Became the Largest Independent E&P Company

ConocoPhillips became a pure-play upstream company in May 2012 when it spun off its refining and marketing operations into a separate company, Phillips 66. This strategic separation unlocked significant value—now 100% of capital flows to exploration and production rather than being distributed across the entire value chain. Under CEO Ryan Lance, who has led the company since the spinoff, COP has consistently acquired high-quality, low-cost assets while maintaining a strong balance sheet.

The company’s geographic footprint spans 14 countries across six operating segments: Lower 48 (Permian Basin, Eagle Ford, Bakken), Alaska, Canada (Surmont oil sands, Montney shale), Europe/Middle East/North Africa (Norway, Libya, Qatar), and Asia Pacific (Australia, Malaysia, China). This diversification distinguishes COP from pure Permian operators like Diamondback and Devon, while its exclusive upstream focus differentiates it from integrated majors ExxonMobil and Chevron.

For investors, the investment case for ConocoPhillips is not merely a bet on the direction of crude oil prices. It is a bet on a specific and highly disciplined philosophy of capital allocation. The core of our buy thesis rests on two distinct pillars:

The “Accretion via Equity” Strategy: A demonstrated history of utilizing its premium-valued equity currency to consolidate assets during industry troughs, followed by aggressive share repurchases to drive massive growth in production per share.

The Global Gas Pivot: A structural advantage in the global Liquefied Natural Gas (LNG) trade, positioning the company to serve the escalating baseload energy needs of the digital economy (datacenters) while capitalizing on arbitrage opportunities that pure-play domestic producers cannot access.

This report provides an exhaustive analysis of ConocoPhillips’ business model, financial health, asset integration, and strategic trajectory. We will dissect the mechanics of its recent acquisitions, the integration of Marathon Oil, the economics of its Alaskan and global gas portfolios, and the rigorous financial framework that underpins its distribution strategy.